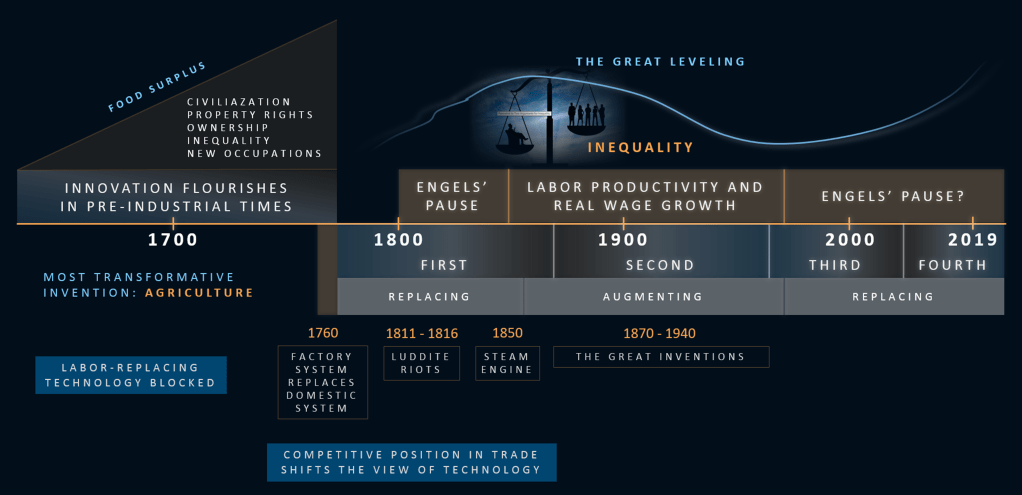

One of the more eye-opening narratives in the story arc of my presentation is the comparison of our current era to the 1920s. Given the catastrophic period that followed, lessons can be learned. A great period of invention ran in parallel, helping to establish our modern standard of living. But there was another period of invention that is also very instructive. That period dates to the early 19th century and is closely associated with the Luddite movement and the birth of the factory system. In a book released this September, Brian Merchant explores this period in history and its similarities to our current era. If the 1920s sowed the seeds of the conflicts that followed, the early 19th century sowed the seeds of labor movements, the modern welfare state, and of all things, science fiction.

(more…)Tag: Labor

-

The Changing Human Life Cycle

Given the recent focus on demographics, I went back to review a book in my library titled “The Great Demographic Reversal.” In a post that reviewed the book, I mentioned that the authors state several times that their findings are controversial and counter to the views of mainstream economists. By way of review, the authors concluded that the future is one of:

(more…) -

The Looming Labor Shortage

In a post yesterday on population growth, I shared a fascinating visual that looked at the age structure of our population in 2017 versus projections for 2100. The tweet is shared again below, click on arrow in the visual to see the changes.

Population size is important in several ways. Historically, experts worried about societies ability to sustain an ever-growing population. With climate change issues mounting, those concerns remain. However, a scenario where our global populations shrink brings a different set of challenges. As this article on projected labor shortages describes, the growth rate of an economy is determined by two factors: growth in hours worked and growth in productivity. The sustained economic growth of the last 250 years can be attributed to a growing skilled workforce (education played a major role) and major innovations that drove productivity.

(more…) -

The Profit Paradox

I finished another book and added it to my book library. The Profit Paradox was written by economist Jan Eeckhout and focuses on the decline of competition in the market. This decline, and the resulting dominance of large firms, has contributed to inequality, reduced innovation, and dropped the labor share of the economy.

(more…) -

The Great Demographic Reversal

Beginning in 1990, several forces converged to shape the global economy. Globalization, demographics, technology, deflation, debt, and interest rates have all played a role. Now, according to a recent book, at least two of those forces are reversing. In The Great Demographic Reversal, authors Charles Goodhart and Manoj Pradhan describe these forces and their influence on the last thirty years of economic activity. With this convergence, the world experienced an extended deflationary period, which per the authors, was driven in part by a labor supply shock. The book said the following:

(more…) -

Technology Trap

I recently added a fascinating book titled Technology Trap to my Book Library. Author Carl Benedikt Frey has done some important work in partnership with Michael A. Osborne evaluating the impact of automation on the Future of Work. In this new work of applied history, Frey draws on past revolutions to look at possible corollaries. It was Winston Churchill that said: The further Backward you Look, the Further Forward you can See. That quote has stuck with me, prompting my Looking back to see Ahead. Here is the book abstract:

-

The Journey Continues

It’s been over a year since launching an Online Course focused on a complex and uncertain future. The course takes a Journey through the Looking Glass – a metaphorical expression that means: on the strange side, in the twilight zone, in a strange parallel world. It comes from the Alice and Wonderland literary work of Lewis Carroll, where he explores the strange and mysterious world Alice finds when she steps through a mirror. I have always found this to be a perfect metaphor for our times.

Every time the looking glass has appeared, the world has experienced a Tipping Point. While I firmly believe a tipping point is coming, the impact is likely a question of severity. Some believe that we have survived similar economic transitions in the past, while others disagree:

-

The Turbulent 2020s and what it Means for 2030 and Beyond

In a recent insights report, authors Karen Harris, Austin Kimson and Andrew Schwedel look at macroeconomic forces and their impact on labor in 2030. The Collision of Demographics, Automation and Inequality will shape the 2020s – a collision that is already in motion. By 2030, the authors see a global economy wrestling with a major transformation, dominated by an unusual level of volatility. Here’s a summary of these three forces:

AN AGING WORKFORCE

As the global workforce ages rapidly, our authors forecast a slowing of U.S. labor force growth to 0.4% per year in the 2020s, thereby bringing an end to the abundance of labor that has fueled economic growth since the 1970s. Even as longer, healthier lives allow us to work into our sixties and beyond, it is not likely to offset the negative effects of aging populations. This labor force stagnation will slow economic growth, with negative side effects including surging healthcare costs, old-age pensions and high debt levels. On the positive side, supply and demand dynamics could benefit lagging wages for mid-to-lower skilled workers in advanced economies through the simple economics of greater demand and lesser supply – but that leads to their second major force: automation.

-

No Ordinary Disruption

In my last future of business series post, I focused on a recent book titled No Ordinary disruption. That post explored the author’s belief that our intuitions must be reset. In that same book, the authors explore what they call “trend breaks”, or shifts away from the trends of the recent past. This post will look at these breaks and their impact on 21st century organizations – and it starts with value. In the rapidly growing world of ecosystems, the way value is created and captured is changing. But, more fundamentally, even our traditional views of value are being challenged. The authors use GDP as a way to underscore this point. They estimate that digital capital is now the source of roughly one-third of total global GDP growth, with value delivered via intangible assets like Google’s search algorithm or Amazon’s recommendation engine. Even our long standing view of capital itself is shifting, as human creative capital becomes a critical source of value.

Additionally, future value increasingly accrues to consumers. In a recent article titled Why Every Aspect of Your Business is about to Change, the author talks about the destruction of value for incumbents and the creation of value for consumers in the form of consumer surplus. They use a powerful example to make their point: Skype brought in $2 billion in 2013, but McKinsey calculates that at the same time, they transferred $37 billion away from telecom firms to consumers via free or low-cost calls. Even the innovative new company only gets a fraction of the value created (Skype: $2 Billion, Consumers $37 Billion). So back to value and GDP: consumer surplus is not accounted for in the way we measure GDP. This creates two challenges: First, do we need to change the way we measure value? Second, how do companies monetize the newly created consumer surplus?

So what does this mean for the future of business? Let’s start with something right from the aforementioned book: On the first day of classes at Ivy League colleges, it was common for the dean to warn students: “Look to the left, look to the right. One of you won’t be here next year.” That seems very appropriate when looking through the lens of company viability. This real phenomenon unfolds over the next decade, driven in part by several trend breaks as identified by the authors: