In my last future of business series post, I focused on a recent book titled No Ordinary disruption. That post explored the author’s belief that our intuitions must be reset. In that same book, the authors explore what they call “trend breaks”, or shifts away from the trends of the recent past. This post will look at these breaks and their impact on 21st century organizations – and it starts with value. In the rapidly growing world of ecosystems, the way value is created and captured is changing. But, more fundamentally, even our traditional views of value are being challenged. The authors use GDP as a way to underscore this point. They estimate that digital capital is now the source of roughly one-third of total global GDP growth, with value delivered via intangible assets like Google’s search algorithm or Amazon’s recommendation engine. Even our long standing view of capital itself is shifting, as human creative capital becomes a critical source of value.

Additionally, future value increasingly accrues to consumers. In a recent article titled Why Every Aspect of Your Business is about to Change, the author talks about the destruction of value for incumbents and the creation of value for consumers in the form of consumer surplus. They use a powerful example to make their point: Skype brought in $2 billion in 2013, but McKinsey calculates that at the same time, they transferred $37 billion away from telecom firms to consumers via free or low-cost calls. Even the innovative new company only gets a fraction of the value created (Skype: $2 Billion, Consumers $37 Billion). So back to value and GDP: consumer surplus is not accounted for in the way we measure GDP. This creates two challenges: First, do we need to change the way we measure value? Second, how do companies monetize the newly created consumer surplus?

So what does this mean for the future of business? Let’s start with something right from the aforementioned book: On the first day of classes at Ivy League colleges, it was common for the dean to warn students: “Look to the left, look to the right. One of you won’t be here next year.” That seems very appropriate when looking through the lens of company viability. This real phenomenon unfolds over the next decade, driven in part by several trend breaks as identified by the authors:

Emerging Middle Class – new markets are growing and fragmenting into many segments, creating a $30 trillion consumption opportunity by 2025 – and emerging markets will grow 75% more rapidly than developed economies. This trend break from developed to emerging economies is driven by the forces of industrialization, technology, and urbanization, driving incomes higher for billions of people, lifting 700 million out of poverty and adding 1.2 billion new members to the consuming class (3 billion by 2025). To win in these markets, a re-imagining of resources, capabilities, and operations is required. Products and services from developed markets cannot simply be transplanted into emerging markets. The focus must shift from regions and countries to cities and urban clusters. Products and prices will be customized to meet local tastes, and faster, lower-cost supply chains are required. Innovative business models and re-imagined marketing and sales strategies will emerge, while organizational structures, talent strategies, and operating practices will transform.

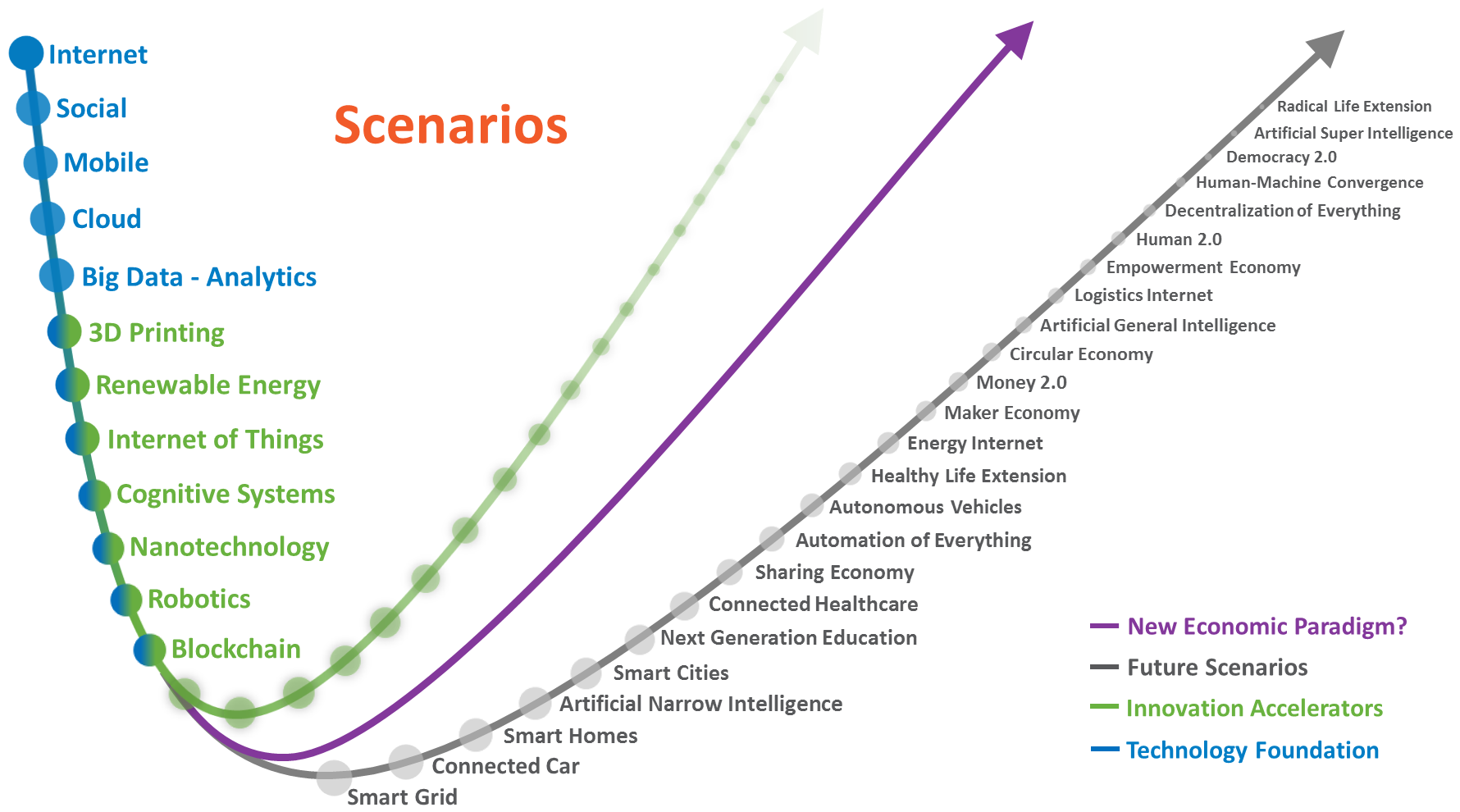

Resources – the industrialization and urbanization of emerging economies has triggered soaring demand for energy, food, and natural resources, at a time of increasingly difficult and costly supply. The trend break here is a shift from falling commodity prices in the twentieth century to doubling on average between 2000 and 2013. The authors believe there are four major drivers of rising prices that keep them volatile in the years ahead: rising demand, depleting supply, resource inter-connectivity, and environmental costs. Let’s take a look at demand for example. The authors expect the global fleet of passenger cars to increase from approximately 1 billion vehicles today to 1.7 billion by 2030. That drives a need for roughly 6.8 billion tires, and likely keeps the prices of natural rubber climbing further. So is the driverless car and sharing economy intersection on our Future Scenario curve a necessity versus a disruptor? Kenneth Rogoff, professor of economics and public policy at Harvard University states that the demand shift from integrating 2.5 billion people from China and India alone will put more upward pressure on commodity prices.

Capital – Weak global demand for capital is unlikely to continue, representing a trend break towards more expensive capital. The authors point to the need for emerging economies (Brazil, China, and India) to increase infrastructure investment to keep up with demand driven by urbanization and population growth. Meanwhile, advanced economies must address years of pent-up under-investment to improve the capacity and service levels of existing infrastructure. The authors provide two future scenarios to describe how this may develop: a higher cost of capital, or a more volatile system. They advise that regardless of which scenario unfolds, an intuition reset is required in the way capital is managed. They provide five actions that will help companies emerge healthier: capital productivity, new sources of capital, new commercial opportunities, managing risk through flexibility, and changing your mindset.

Dislocation in the labor market – This trend break speaks to the expansion of automation beyond routine transaction jobs to jobs that require personal interaction, problem solving, and a range of critical thinking skills. The authors describe how technology is being used to disaggregate jobs into specialized tasks at a granular level, with flexible labor working remotely (a key driver of the independent work force movement). Labor force participation in America continues to decline (2014 was a 36 year low), and technological churn renders new skills outdated at an ever-faster pace. The growing skills gap is intensifying, as a global shortage of approximately 40 million high-skilled workers and 45 million medium-skill workers may emerge, by 2020. This skills gap sits alongside a surplus of 95 million low-skilled workers. Yet, we see a paradoxical situation where we have a shortage of high-skilled labor amid a difficult job market for college graduates. At the heart of this paradox is a void in qualified applicants in the STEM related fields, as only 15 percent of US graduates pursue majors in these fields. In a world with increasing skill shortages, the focus must shift to improving labor productivity. For example, organizations could realize improvements in knowledge-worker productivity by about 20 percent using digital technology.

Rise of New Competitors and a Changing Basis of Competition – a convergence of forces is transforming global competition and blurring the boundaries between sectors. Technology and inter-connectedness are enabling emerging-markets on the world stage, and shifting the balance of power between large, established companies and smaller, nimbler start-ups. This is a trend break from a global competitive landscape where the developed world giants dominated and fought with well-known competitors (Ford vs. General Motors, Coca-Cola vs. Pepsi, etc.). Instead, collapsing barriers to entry enable smaller competitors with access to digital platforms that are born global, and can scale up quickly. In this world, advantage shifts to new competitors that leverage emerging platforms, business models, and competencies. Established firms playing by old rules of competition will need to reset their intuition to compete effectively. But it’s not just the nimble start-up. By 2025, 230 emerging market companies are expected in the Fortune Global 500 – up from 130 in 2013, and the number of large companies based in these countries could increase from 2,200 today to around 7,000. In the future, business must re-think their traditional competitor set, monitor new competitors, and strive to understand the economics and business models of new industries.

Challenges for Society and Governance – the creative destruction happening all around us is not simply a business issue. Governments will be pressed to respond faster, with a level of political maturity and leadership needed to navigate through a massively transformative future. Governments will be challenged to address labor, trade, immigration, and fiscal policy, in an era of declining budgets and rising debt. As business leaders reassess their strategy and reimagine their business assumptions in the face of these trend breaks, government will do the same. The authors explore three questions about the nature of government in the future: the size of government, the degree to which it should be centralized or localized, and its overall role. They probe on the use of incentives and regulation to both accelerate and manage change.

These trend breaks are a reminder that although technology is enabling these breaks, there are multiple converging forces altering the future of business. As you digest the trend breaks articulated above, view them through the lens of a radically different future, and leverage foresight and Future Thinking to explore the ramifications to your organization. I’ll continue the focus on the future of business in my next post.

{kind=link}

Leave a comment