I had a great discussion today with David Cohen, Founder, and Chairman of E7 Ventures. Our topic was the future of energy and his belief that we are rapidly heading towards an Energy Internet. Like most other areas of science and technology, energy is experiencing an exponential progression that likely changes the energy paradigm in the coming decade. In his book titled The Zero Marginal Cost Society, Economist Jeremy Rifkin describes how Internet technology and renewable energies are merging to create an energy Internet that changes the way power is generated and distributed in society – a paradigm shift in energy similar to what occurred in computing. He describes an emergent system with synergies between Five Pillars that drive this paradigm shift:

- Shifting to renewable energy

- Transforming buildings into micro–power plants to collect renewable energies on-site

- Deploying hydrogen and other storage technologies to store intermittent energies

- Using Internet technology to transform the power grid into an energy Internet

- Transitioning the transport fleet to electric plug-in and fuel cell vehicles that can buy and sell green electricity on a smart, continental, interactive power grid

Given the power of this shift, I wanted to get David’s thoughts on its timing and impact. We explored his current view of renewable energy and those likely to accelerate. David sees solar energy as the dominant renewable, and mentioned that the energy internet – and solar in particular – will scale up much faster than people believe – which is a good thing, given that he mentioned energy demand doubling by 2030. In his words, the next ten years is where all the change will happen.

The rest of our dialog focused on solving storage issues, the role of Blockchain in creating an energy internet, and the likely path of the incumbents (part protectionism and part innovation).

You can listen to the full 25 minute podcast below.

A PDF version of the infographic is available here.

A PDF version of the transcript is available here.

A transcript of our discussion follows

Edited for clarity

FRANK DIANA: Hello, this is Frank Diana with Tata Consultancy Services and I’m joined today by David Cohen, Founder and Chairman of E7 Ventures. Our topic today is “The Future of Energy.” Before getting started with this podcast, I’m going to first invite David to introduce himself. David if you would.

DAVID COHEN: Hi Frank. Thank you for having the podcast. My name is David Cohen. I’m an entrepreneur in the Smart Grid space. I’ve been, for the past 25 years, building software around a highly decentralized energy system. I’ve built four startup companies, from vision, launch, scale, to exit, and I’ve built a lot of commercial software products. In actuality, many industry firsts, including one of the first automated demand response platforms, at a company called Infotility. I built the first decentralized, peer-to-peer energy sharing smart grid platform called GridAgents™, which was used globally and at Con Edison, in Manhattan. Right now, I’m the COO of ZipPower, which is developing a new platform called The Community System that allows smart cities to essentially become platforms to build solar plus energy storage microgrids. I’m really passionate about distributed energy, if you can’t tell, but most of my work has been around software, communications and controls for distributed energy systems. I’m really looking forward to moving and evolving that, as it’s a very exciting space. Thanks.

FRANK DIANA: Great and given your background, this will make for a good conversation. I wanted to start our dialogue around the notion of an “energy internet” which Jeremy Rifkin talked about in his book “Zero Marginal Cost Society.” In it, he talks about how internet technologies and renewable energies are merging to create this energy internet, and shifting the power generation and distribution paradigm. What are your thoughts on this notion of an energy internet? Is it a new notion or this is something we’ve been looking at for a while?

DAVID COHEN: I might jump around a little bit, but I think the energy internet is here, as we speak.

What is the energy internet? Essentially, it links a highly distributed energy resource system, where you have solar on buildings, fuel cells and different types of distributed energy technologies connecting to the grid with information. The whole concept of [energy] internet has been talked about since the EPRI (Electric Power Research Institute) IntelliGrid and the Department of Energy. I was a founding GridWise Architecture Council member that helped define the standards for transactive energy and “what the smart grid needs to do.” It’s really about combining information, analytics and power, flowing locally and bi-directionally, and it’s happening, as we speak. In terms of the scale, the energy internet is going to scale out much faster than people believe. I know that you also wanted to talk about what type of things are happening, what’s driving this and I can get to that in a different question, if you like, and stay on the energy internet. Part of answering your question though has to look at what’s happening and what had happened in the last couple of years that are really driving this.

FRANK DIANA: Well, why don’t you get into that. So give us a little background. What is driving this?

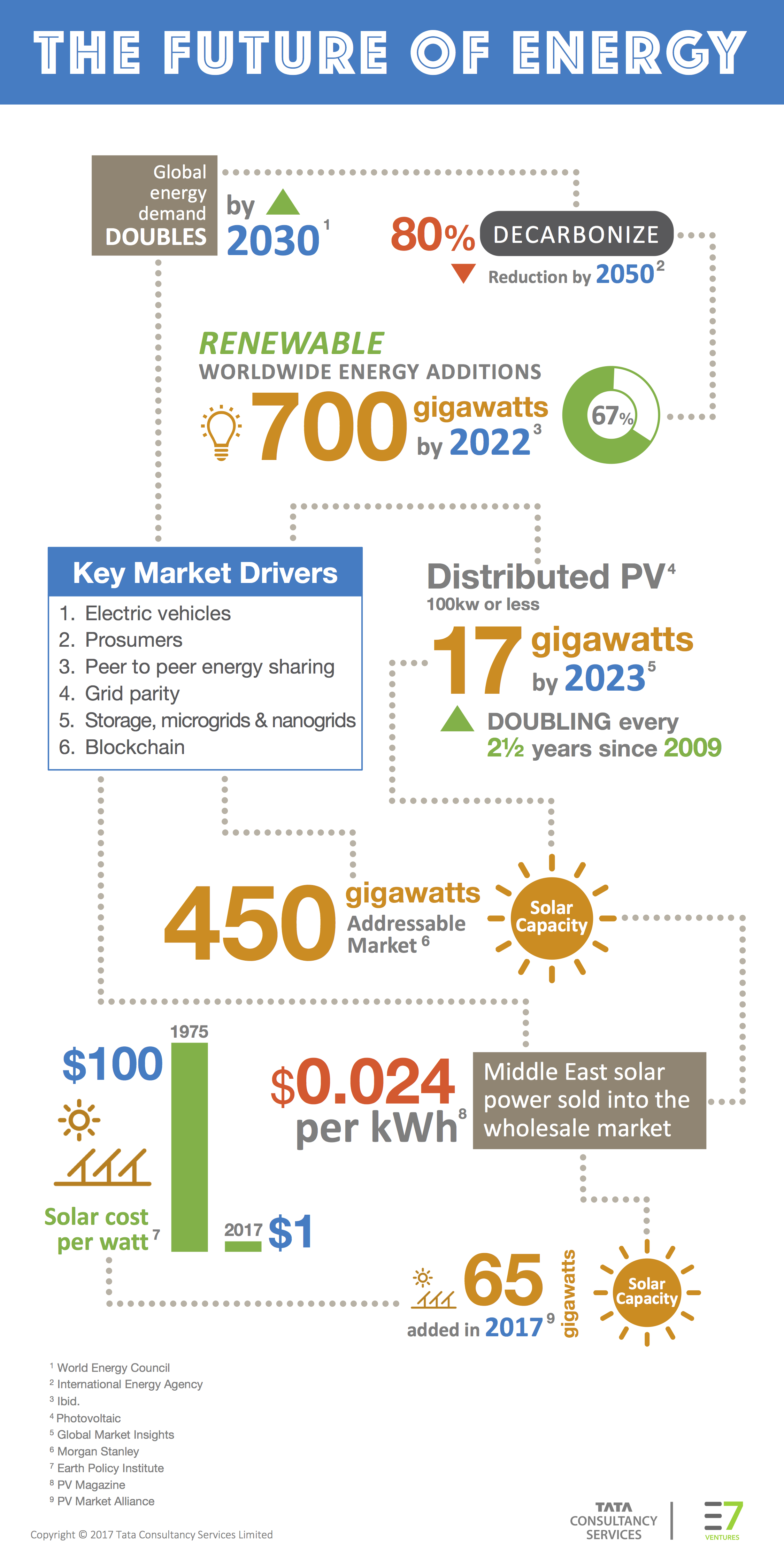

DAVID COHEN: A lot of people may not realize, but the global energy demand is going to double more or less by 2030.1 The fossil fuel prices and the large-scale power plants–the nuclear, the natural gas and coal, those prices are rising and renewables are declining rapidly. So, this concept of “grid parity” is happening globally, where the ability to produce power with smaller scale renewable power sources is reaching almost every country on the planet and it’s happening very quickly. Renewable energy, electricity additions over the next five years is going to be over seven hundred gigawatts.2 That’s almost two thirds of the net additions to the global power capacity, according to the IEA, the International Energy Agency. As part of that, distributed solar PV [photovoltaic] is one of the bigger drivers and that capacity, of say a hundred kilowatts and less, is estimated to exceed seventeen gigawatts by 2023.3 Essentially, the whole distributed PV market started about 2009 and it’s been doubling about every two and a half years. Morgan Stanley estimates there’ll be 450 gigawatts over the next five years.4 If you look at the uptake curves, you really have to understand that back in 1975 the price of solar was $100 a watt and now it’s going at less than $1 a watt.5 There was a record breaking solar plant in the Middle East where they’re selling utility scale solar at $.02 a kilowat hour, plus or minus a little bit and that’s less than any power plant to date has sold into the wholesale market.6 So, that’s the tip of the iceberg.

The other thing that’s really driving this and what everybody is really talking about is decarbonization, and whether we’re going to decarbonize 80% by 2050. We’re talking about, almost full decarbonization of power, road transport and buildings. Those are all the areas that I’ve worked on, but if you look at what’s going to happen there, it gets into energy storage and electric vehicles, which we’ll talk about later. All those things–prosumers, the emergence of peer-to-peer energy sharing, and a more highly decentralized system is leading to this idea that all of this is happening faster than anyone though. If you go back to 2005, distributed solar was almost miniscule and not even on the graph. The last ten years is where everything’s happened and the next ten years is going to be the game changer for distributed energy. If you look at the European Union, Germany and other northern European countries, what’s happening and how much solar they have distributed and utility scale renewables, as well as California’s DERP, and New York Reforming the Energy Vision (REV)–all those are promoting and assuming high penetration of distributed energy resources have to be integrated into the grid.

There’s also another game changer that happened only a few months ago. The Federal Energy Regulatory Commission (FERC) ordered all of the independent system operators (ISOs) to accept energy storage and aggregated distributed energy resources as into the market. They did this a few years back with demand response, but they’re basically now saying that anything can produce power locally can participate in the ancillary services markets. If you’re a prosumer, the market will have to come up with a way to accept that capacity and come up with pricing mechanisms. If you think about the last ten years, the next ten years are going to, where all that change is going to happen. So, when you say energy internet, it is here. The fundamental thing behind the energy internet, just like the internet itself, having smart routers that route the information around, lots of servers that produce and store huge amounts of data and a very fast internet backbone that can transfer information. The energy internet is going to require smart power electronics which you’re starting to see inside of very sophisticated smart solar inverters and microgrid controllers. These inverters can provide all kinds of services and very fast controls. Some of the newer things that are happening are going to make this really scale–very, very fast time scale changes to electrical power characteristics from these smart inverters and microgrid controllers. So, I give Jeremy a lot of credit for being a visionary and seeing it, like Amory Lovins has done in the industry, where he sees the future. When you talk about it now, it’s really a matter of “how fast is the energy internet going to accelerate versus is there going to be one?”

FRANK DIANA: Well, great stuff. So, my takeaway is that energy is experiencing the same exponential progression as other science and technology innovations. That seems clear. The renewable energy side of this discussion, like solar, like vertical wind, like geothermal pumps, etc. Are all those things combining or is there one front-runner in terms of renewables?

DAVID COHEN: Well, the front-runner because it’s solid state and because of the cost reductions is solar. It’s similar to the automobile industry, where there’s been a fight about–“should it be diesel?”, “should it electric?”, “should it be hybrid electric?”, “should it be fuel cells?” What’s going to win, because it’s the most elegant technology, is electric vehicles with batteries because that’s the easiest thing to do. Fuel cells are beautiful technology, but I don’t know if they’re going to make it. The same thing with renewables. I think we’re going to continue to see very large-scale solar, very large-scale wind, and large-scale hydro, which has been mostly what we’ve seen so far. When it comes to what’s going to be on the localized basis, there have been discussions about micro turbines, and small micro CHP [combined heat and power]. All of that will probably be much more relevant in the EU, but in the United States the grid parity on the solar is going to drive very, very high penetration of distributed PV. In cases where you cannot put PV on the building infrastructure, on the roof, or on a carport, what’s going to happen is community solar, virtual net metering, and other ways of doing virtual sharing. It is going to really drive solar. If you look at utility scale solar, there’s been a lot of talk about concentrating solar and solar integrated with storage and so on, but what really ends up winning at the end of the day is just straight solar. Now, we haven’t talked about energy storage yet because that’s the other large thing that’s going to influence this.

FRANK DIANA: Yes, and before we get into the storage conversation, you’ve mentioned Europe a couple of times. Is there a region in the world that’s further ahead?

DAVID COHEN: I think Germany and most of northern Europe is a little further ahead. I think they have a different view though because they did a lot more distributed combined heat and power systems, where we’re not talking about very small-scale stuff yet. They have more distributed energy and put in almost too much centralized solar and wind, so they’re having a grid balancing problem. Now that’s going to lead to our discussion, when we get to energy storage. The next five to ten years is when the race for distributed energy is going to start. There are a lot of places in addition to California and the East Coast of the United States [where] they’re going to catch up very quickly with Grid Parity.

FRANK DIANA: Well, interesting that you mentioned Germany, because Rifkin has been an advisor to the German Chancellor and that’s probably the reason why Germany is a little bit farther in front. We’ve talked storage, so let’s dive into that one. Clearly with solar and wind, the wind isn’t always blowing and the sun isn’t always shining. How do we deal with the storage problem?

DAVID COHEN: Well right now, you can’t talk about storage without getting into the concept of electric vehicles and microgrids. So, the first thing I would say is that when people talk about storage being too expensive, you really have to look at the EV [electric vehicle] dispersion issue. Since the mid-2000s, there’s been a couple of times when the electric vehicle, was killed, literally. There’s a book written about it. Since about 2012, most of the major car OEMs have plans for significant EV infrastructures and have to give credit to Tesla and Elon Musk for really pushing that forward. Back in 2012, the CEO of Volkswagen stated that “diesel was their future.” After what they call “Diesel Gate,” they’re now talking about a 100% EV infrastructure, eventually. I believe that the OEMs are one of the drivers that will drive costs way down. There’s been a couple of glitches in the dispersion of EV’s, but it takes longer than imagined for people to switch their vehicle types. Once the EV infrastructure and charging infrastructure is in place and once there are more offerings, that’s going to accelerate rapidly. That’s going to cause the cost of energy storage to go way down.

Now the concept of microgrids, where solar really started, and the hype about microgrids goes back to the early 2000s. I was part of those discussions with the Department of Energy and some large players. [Key] was this idea of a critical infrastructure microgrid where you have resilience–if the main grid goes down, you’re able to island and very quickly survive for long periods of time. Those are going to be a very small part of the market because they’re very expensive–things like data centers, hospitals, military bases. Those are great, but 99% percent of the market is going to go more towards things like nanogrids, where you have you have renewable energy production and you have things like solar + storage + smart controls. [Solar + Storage) systems can increase self-generation, provide capacity to do peak demand reduction, and save money, but also to bid that capacity into the energy markets and make money off it. Those systems are typically designed for one or two hours of storage ride-through. They’re not designed for two days of operation so if the grid system goes down for that long. Most Solar + Storage systems are mainly for cost reduction right now and as the prices get very, very low, but it’s going to take a long time, then you can have resilient microgrids that can be off grid for a long period, if there’s an outage. I have to say that the IEEE interconnection agreement that talks about what happens when there’s an outage–all that is changing. In the past couple of years, the IEEE 2030.x Standards, and Rule 21 in California are pushing for better ways to integrate microgrids and aggregated DER systems into the utility distribution networks. Right now, for most solar installations, if the power goes out and you have solar on your roof, the solar inverter shuts down in order to protect the grid. It doesn’t do you any good unless you have a dedicated circuit to store energy and put it on a dedicated circuit in your house.

So, those standards are changing now to require that inverters have more capability to support the grid. More people are doing AC-coupled and DC-coupled microgrids that allow you, when the power does go out, to have a small circuit in your house so that you can stay afloat. It’s called survivability, which is getting more and more popular, especially with critical facilities. There’s much talk and hype about this. It’s all about the resilience and the issues around when the power goes out. I think for most people and most utilities that I talk to, they will say, “Well the grid is actually really reliable.” It’s just when it does go out, it’s very inconvenient and can be very expensive for some businesses and so I think a lot of companies and building owners, when the cost gets to the right point, will want to have some storage for those reasons. We haven’t talked about Vehicle-to-Grid (V2G), which got very hyped up, but depending on [whether] the business model is right, V2G could open up a huge market for energy storage that’s mobile and can provide capacity and services to the electric grid. It could be essentially plugged into the system and used as an enhancer to the grid.

FRANK DIANA: So, you see the storage issues getting resolved in this ten-year window that you referenced where the energy paradigm changes considerably?

David Cohen: Yes, if you look at the growth curves of solar and you look at how long it took to get here, it’s obvious that things have accelerated in the last seven years. So if you say that the solar revolution on the distributed PV side happened in the past five to seven years, and you look at how much capital is going into energy storage and look at the electric vehicle infrastructure as a driver. You can imagine the potential for energy storage as you can read in the news. Lazard puts out an energy storage lifecycle cost analysis every six months. The same with the U.S. Energy Information Administration (EIA), Greentech Media, Navigant, and others–they all put out reports, but I think they’re all going to show that they really don’t have a way to estimate this because most of these trends are happening faster than the analysts know how to keep track of [them]. I’ve been looking at this for 25 to 30 years, so I’m not looking at this unrealistically. I’m seeing some very unique things that are changing the dynamics that were not here 10 years ago.

FRANK DIANA: I’m seeing the same kind of progressions in so many other places. So, it’s clear that we’re accelerating past points that we ever envisioned. I’m going to shift gears here quickly and talk about blockchain, a very topical item in the industry today. Talk to me about blockchain and its role in this energy internet.

DAVID COHEN: Okay, I assume people know what blockchain is. It’s a distributed ledger and it uses a cybersecure digital currency. In the case of blockchain, it’s the underlying digital ledger that allows something like bitcoin to work. It was designed initially to have something where there is value being traded–a virtual currency, so that you can pay for something peer to peer. The main aspect of it is that it’s very, very hard to spoof. It’s a trustless network that allows you to do cybersecure transactions and it’s very sophisticated. It’s very energy intensive for the peer computers to actually do the calculations, to verify the network. One of the issues in looking at cyber security in this market is currently the cost to do a transaction. [It] is pretty expensive, if you’re trying to do very small micro transactions.

So, what you’ve been seeing in the market is people trying to come up with new ways to talk about using blockchain with transactions or a currency that has a much lower cost to actually do the transaction. Imagine if you’re trying to sell power between two houses and the transaction cost was five cents a kilowatt-hour, but the value of a kilowatt-hour is only six cents. It’s not going to work. So the real value of blockchain in the energy space (obviously, there are many use cases outside of energy–Fintech and Industrial Internet of Things) and almost everywhere you look blockchain is emerging as a potential disruptor. The real value I see in the energy internet is two areas: one is energy sharing; like some of the great work that was done by TransActive Grid and LO3 .

There’s been some other examples of that but the current work did not include a really important component, which is transactive control. We launched a lot of that through the GridWise Architecture Council (GWAC) with the Department of Energy. We talked about that in the 2005 timeframe, and the GridAgents™ Platform that I built at Infotility was one of the first transactive energy systems in the market. Later, around 2012, the GWAC launched the framework but we should give credit to many others in the industry in making transactive energy what it is today. [It] requires not just cyber secure transactions, but it requires a distributed control framework that can provide sophisticated forecasting and control algorithms embedded locally.

So, where blockchain can really add value is making that distributed, highly decentralized control system cybersecure, without having to rely soley on the centralized grid operators. There’s just not an easy way to look at the emerging SmartGrid system, [given] how complicated it is in a highly distributed way and monitor it from a centralized control center. You have to have something that you can trust. I think, at this stage of the game, there’s been a lot of stuff that’s been talked about, but the real trust issues are not going to get resolved until they become standards, at least for the energy space. The Smart Grid is run by international standards bodies. Something like an Ethereum approach, where it was attacked, will not be acceptable to major utilities. If you have unregulated subsidiaries (of utilities) that are going out and building energy service companies, they’re still going to have the same issues. Any breach of security is going to be a big problem and I think that where blockchain really shines is its ability to have a much more promising way to have trust (as an addition to a robust cybersecurity policy and framework).

FRANK DIANA: That’s great. Sounds like the right approach. I’m going to ask one very quick question, before we close. Given all this, there’s obviously a disruptive impact to incumbents. How do you see incumbents responding over next several years?

DAVID COHEN: I see two things. One is that we might see some hyper-regulation or at least having incumbents trying to get into the regulatory process to slow down some of this highly distributed energy system because utilities are regulated to actually get return on their assets from investing in more centralized systems. They need to understand how DER systems and Microgrids will impact grid reliability. I think they want to be on the distributed side; they’re not ready to do it yet. So, they’re going to get involved in regulations that allow them to slow it down, so they can catch up. We have already seen the unregulated subsidiaries of these very large investor-run utilities making huge investments and doing M&A in preparation to become the operators. Maybe not from a regulatory standpoint, but maybe a deregulated business model.

If you’ve heard of the concept of “distribution system operator (DSO), it’s really being designed to manage this high penetration of distributed energy systems. And so, I would close with two things. (1) They’re going to regulate and try to come up with rate structures to slow it down or to make sure that they can actually return value to their investors, and (2) at the same time, they’re going to prepare for the ultimate change in the way that the system is going to be managed, which means their generation assets are not just privately held somewhere at the front of the meter. They’re going to exist everywhere (behind the meter, centralized, distributed, and networked) and that’s the major change underway, its Utility 2.0.

FRANK DIANA: So one part protectionism, one part innovation.

DAVID COHEN: Yes. I worked on one of the first net metering [initiatives]. I guess it was the second, because California pioneered it. A guy named Howard Wenger pioneered the California net metering program. We actually went to the same engineering program at the University of Colorado. In the late 90s, I guess mid-90s, an attorney, named Ron Lehr, and I pushed net metering policy in Colorado. At the time, it seemed like a really great idea, but the utilities weren’t ready for it. It wasn’t their idea, so they fought it and then they initiated it themselves a couple years later. Ron Lehr was the one who gave me this idea of hyper-regulation. He said, “When this stuff happens, from an attorney standpoint and from a regulatory standpoint, it doesn’t go into less regulation, it goes into more regulation” and I think that’s what we’re going to see.

FRANK DIANA: Interesting. Well, we are out of time David. I appreciate you spending time with us today. Why don’t you to tell the audience how they can reach you, if they’re interested in following up.

DAVID COHEN: Sure, my e-mail is dc@evolution7.net and I have a website, http://www.e7ventures.com. Mainly, you can contact me through e-mail. You can also reach me at David@ZipPower.com, or at www.zippower.com.

FRANK DIANA: Great. Yes and for those listening, you can reach me either at TCS.com or my blog frankdiana.net. David thank you again for joining us.

DAVID COHEN: Thank you.

References:

- Global Energy Demand to Double by 2030 https://www.theguardian.com/business/2016/oct/10/global-demand-for-energy-will-peak-in-2030-says-world-energy-council

- Renewable electricity additions over the next five years will top 700 gigawatts (GW) that will account for almost two-thirds of net additions to global power capacity

https://www.iea.org/newsroom/news/2015/october/renewables-to-lead-world-power-market-growth-to-2020.html

- Distributed PV Solar systems with production capacity of 100 kilowatts and less Estimated to exceed 17 Giga watts by 2023

https://www.gminsights.com/industry-analysis/distributed-solar-pv-market

- Addressable distributed solar market in US could be 415GW

https://cleantechnica.com/2014/03/25/going-grid-nears-tipping-point-morgan-stanley-reports/

- Solar at $100/watt in 1975, now $0.61/watt

https://cleantechnica.com/2016/02/12/is-this-the-best-solar-chart-yet/

- Utility Scale Solar beat a WORLD record recently selling into the Wholesale at 2+ cents kWh

https://www.pv-magazine.com/2016/09/19/breaking-world-record-low-price-entered-for-solar-plant-in-abu-dhabi_100026145/

Leave a comment